Navigating health insurance can be confusing, especially when faced with terms like copays, coinsurance, and out-of-pocket costs. These concepts are crucial to understanding how much you will actually pay for medical care, beyond just the monthly premium. While health insurance helps protect against expensive medical bills, it’s important to grasp how these cost-sharing elements work, so you can budget accordingly and avoid surprises when you receive your bill.

A copay is a fixed amount you pay for a covered healthcare service, usually at the time you receive the service. For example, a doctor’s visit may have a copay of $25, meaning you pay $25 each time you see the doctor, and your insurance covers the rest. Copays are typically straightforward and predictable, which makes it easier for insured individuals to plan for routine expenses such as doctor visits, specialist consultations, or prescription medications. However, the amount of the copay varies depending on your insurance plan and the type of service. Some plans might require higher copays for specialist visits than for primary care, and emergency room visits usually come with a higher copay as well.

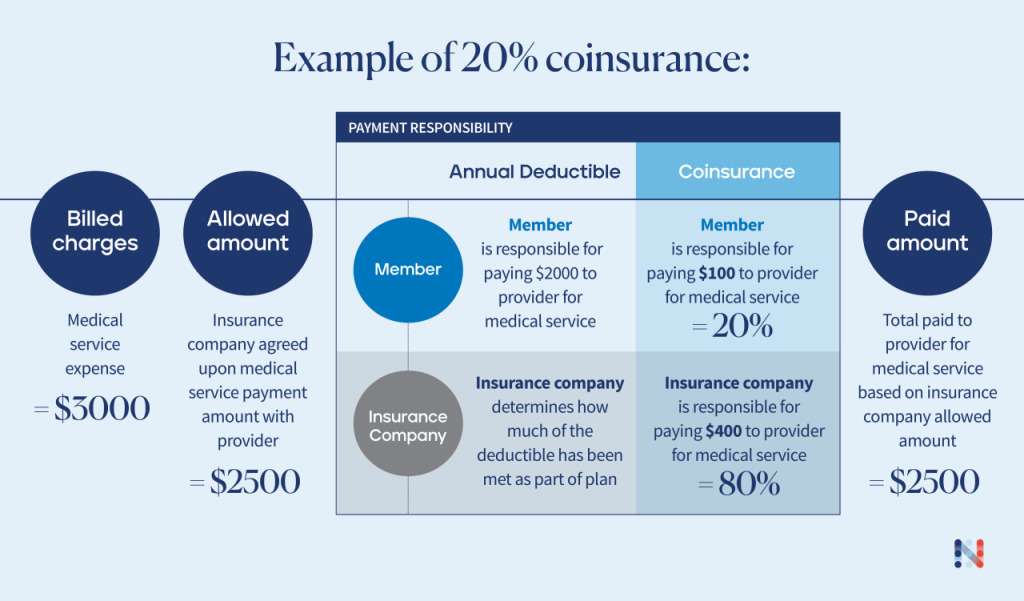

Coinsurance, on the other hand, is a percentage of the cost of a covered service that you are responsible for paying after meeting your deductible. Unlike copays, which are flat fees, coinsurance means you share the cost with your insurance company in a specified ratio. For instance, if your plan has 20% coinsurance, and you receive a medical bill of $1,000 after your deductible is met, you would pay $200, and your insurer would cover the remaining $800. Coinsurance applies to services like surgeries, hospital stays, and diagnostic tests, and it can lead to variable out-of-pocket costs depending on the service’s total charge. Because coinsurance is percentage-based, your actual payment can fluctuate significantly, making it harder to predict your expenses compared to copays.

Both copays and coinsurance contribute to your out-of-pocket costs, but these out-of-pocket expenses have limits. Most health insurance plans have an annual out-of-pocket maximum, which is the most you will have to pay during a policy period (usually a year) for covered services. Once you reach this limit through copays, coinsurance, and deductibles, your insurance covers 100% of covered benefits for the rest of the year. This cap is designed to protect you from catastrophic medical expenses and provides financial security during times of extensive medical care.

It’s also important to understand the deductible, which is the amount you must pay out of pocket before your insurance begins to cover a portion of your medical costs. Deductibles work hand-in-hand with coinsurance. Until you meet your deductible, you generally pay the full cost of services, except for those requiring copays, depending on the plan. After satisfying the deductible, coinsurance kicks in. Some insurance plans feature separate deductibles for different services or family members, which can further complicate how costs add up.

The distinction between in-network and out-of-network providers also plays a significant role in your copays, coinsurance, and overall out-of-pocket costs. Insurance companies negotiate lower rates with in-network providers, which means your cost-sharing amounts are generally lower if you stick with these providers. Out-of-network providers usually come with higher coinsurance rates, copays, or sometimes no coverage at all, resulting in larger bills. Being aware of your network status before receiving care can save you substantial money and prevent unexpected charges.

Prescription drug coverage is another area where copays and coinsurance are commonly applied. Many health insurance plans include formularies, which categorize medications into tiers. Generic drugs often have the lowest copays, while brand-name or specialty drugs may require higher copays or coinsurance percentages. Understanding your plan’s pharmacy benefits can help you manage medication costs and avoid surprises at the pharmacy counter.

When choosing a health insurance plan, it’s essential to consider how copays, coinsurance, deductibles, and out-of-pocket maximums interact. Plans with lower monthly premiums tend to have higher deductibles and coinsurance, meaning you pay more when you actually use medical services. Conversely, plans with higher premiums often have lower cost-sharing amounts, offering more predictable expenses but at a higher upfront cost. Balancing these factors according to your health needs and financial situation can help you select the best plan.

Financial assistance programs, such as subsidies through the Affordable Care Act, can help lower your premium costs, but they don’t necessarily reduce copays or coinsurance amounts. Therefore, it’s wise to evaluate your expected healthcare usage and consider how much you are willing to pay out of pocket when you seek care. Using online calculators and consulting with insurance professionals can provide clarity and help you forecast expenses.

Understanding copays, coinsurance, and out-of-pocket costs empowers you to make informed decisions about your health insurance coverage and healthcare choices. Being proactive about these costs can prevent surprises and ensure you are financially prepared when you need medical care. Taking time to review your health plan’s summary of benefits, asking questions, and planning for potential expenses helps you navigate the complex healthcare system more confidently.

In summary, while premiums are the regular payments you make to maintain health insurance, copays and coinsurance are the cost-sharing components that affect how much you pay at the time of service or afterward. The deductible is the amount you pay before coinsurance begins, and all these expenses contribute to your total out-of-pocket costs, which have an annual maximum limit. Grasping these concepts enables you to better manage your health expenses and choose a plan that fits your financial and medical needs. Ultimately, being informed leads to better healthcare decisions and peace of mind.